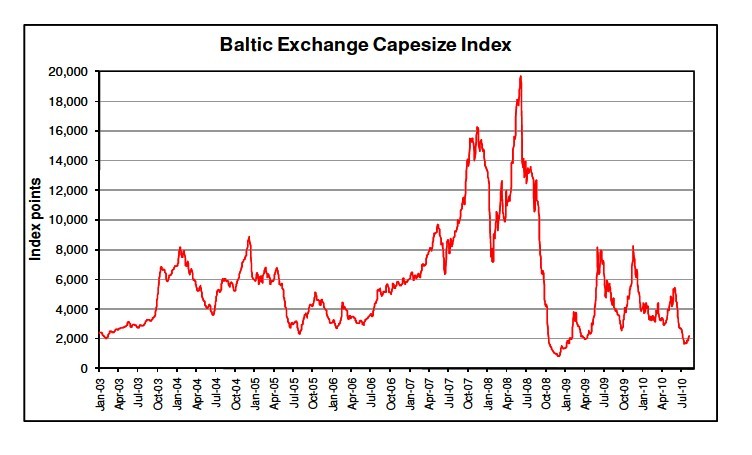

Throughout the week we have seen increased activity across both basins but it

wasn't until the second half of the week that we saw levels pushing forward. With

support shown on the forward position, increased fixing helped to clear out some of

the tonnage in the pacific and fronthaul including columbia coal stems which

enhanced the market to end on a positive note. As the week ended we saw a stand

off from owners as they raised their ideas for fixing. The BCI Index improved up to

2194 at the close of the week, whilst the Average of the Timecharter Routes also

increased by 18.76% up to $18,422 daily.

Early week we saw a slight increase in the number of fronthaul stems being

marketed for second half August and some creeping into early September. With a

number of vessels still ballasting rates for fixing mwere relatively flat but in the

second half of the week the fronthaul market looked tighter and we saw levels

improve circa $1.50 from early week with $21.50 being concluded at the close. The

Tubarao/Qingdao bid vs offer spread closed the week at circa $21.50 vs $23.25

pmt level basis second half August dates in Brazil.

In the East early week tonnage far exceeded demand but as the week progress we

began to see this balance and levels appeared stronger as the week ended. The iron

ore majors took vessels at circa $7.50 for mid/end August dates. Charterers closed

the week bidding levels of circa $7.50 pmt vs $8.00 pmt basis Port

Hedland/Qingdao for early August dates.

The Period market saw much more activity this week as Charterers seeked tonnage

willing to consider mid usd 20,000 for 4/6 months, with the paper pushing owners

were more willing to work at these levels. The 1 year period market level closed this

week at circa $28,500 daily for a BCI type vessel Delivery in the Far East.

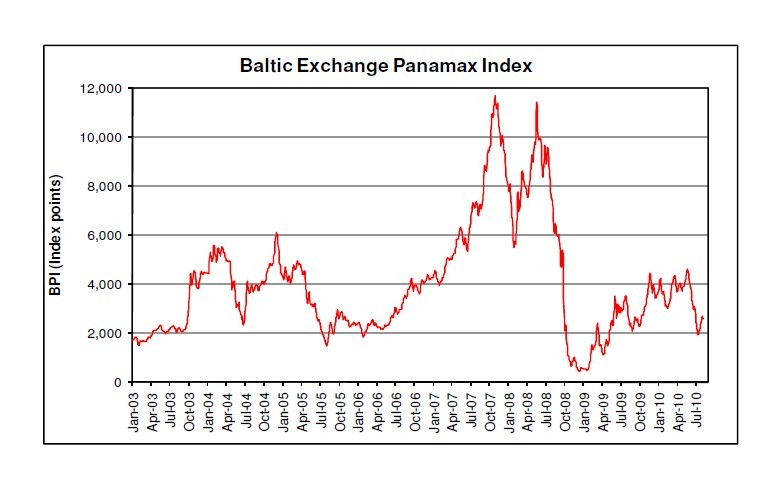

Panamax Atlantic

The market in the Atlantic basin started off fairly quiet and flat this week giving a

feeling that maybe demand is not so strong even though tonnage is still tight in both

the Continent and the Med. However mid-week fresh business especially mineral

cargoes out of the US Gulf 1st half of September heated things up and rates for

transatlantic rounds held firm around $23,000 daily. Rates for 2 to 3 laden legs

redelivery Atlantic pushed up bit more with a ship open Continent rumored to be

fixed around $28,000 daily.

Fronthaul business was less active because of less pressure for east coast south

American cargoes and with a couple of commited vessels in this region and the US

Gulf.

Period business was mainly done in the east but with delivery Atlantic 4 to 6 months

talks were being done in the high $20.000's. It was also rumored a ship being fixed

for 2 years with delivery Atlantic but no further details so far.

Panamax Pacific

We had the usual quiet start to the week where owners and charterers were willing

to watch and wait to see the true direction. Although tonnage was plentiful,

sentiment in the market place was positive throughout the week, rates remained

steady at around 18-19,000usd.

Come mid week, tonnage supply increased for the forward dates, tied in with the ffa

market coming off and a general lack of charterers willing to move, we saw a few

failiures, and owners willing to fix at levels. This was short lived as paper soon

rebounded, with the talk of russian wheat exports being halted, charterers were

keen to take vsls on short period in the hope of seeing longer tonne-miles. Rates for

short period hovered around 23-24500usd for the most part of the week, with a

few employed at around 26,000 ex mide delivery for abt 4-6 months.

The week ended on a strong note, aided by the paper trading strongly. looking into

next week, tonnage supply remains plentiful, however with sentiment very positive

would be difficult to see rates coming off.

Handymax Atlantic

It was a fairly uneventful week across the Atlantic basin, with rates sliding

marginally through-out and a generally flat/slightly weaker tone on both the handies

and supras, resulting in minor falls on the indices. There continues to be a distinct

lack of direction in the Atlantic market at present and although one may assume a

possible further slide into next week, yesterdays official declaration from Russia of

a ban in grain exports for the remainder of the year will clearly have an impact.

Rates in general continued to hold up reasonably well, with TA RV on index types bss

south Cont/Gib dely being concluded at levels around the usd 18k and very low 20's

being seen for those wiling 2ll with Atlantic redely. Again there's still a steady

supply of scrap, steels and ferts cargoes off the continent with levels for Cont/Usg

trips at close to usd 10k and trips to the Med in the high teens. It has to be said

that handysizes are holding up very well and attaining levels not dissimilar to these -

infact slightly above supras for Cont/Usg runs. From the Usg, levels in the high usd

20's for bsi types were being attained for trips back to the Cont/med with rumours

of usd 30k on a 56k for quick trip back to West Med with petcoke being concluded

on subs. Reported short period deals were thin on the gound but generally mid 20's

for 3/5 mnths bss US Gulf delivery and v.low 20's bss Cont/Med deliveries were

attainable. The East Coast South America market showed some resilience with a

considerable number of grains and sugar cargoes available with a level shade above

usd 25k being paid for trip to China bss favourable west africa delivery.

The market is still delicately balanced, and though there remains a number of early

vessels in the atlantic one would hope there's sufficient enquiry to absorb same,

howeever it remains to be seen what affect the Russian grain ban may have in the

short/long term.

Handymax Pacific

A slow start to the week in the pacific, which is not entirely unexpected in August

given that many people are on annual leave/Holidays.

Very few stems left ex Indo before mid August have left rates to come off in Se

Asia, with Smax vsls fixing mid-high teens bss dely S.China and low 20's dely

Indo/Phil for trips to India. East Coast India has faired better in maintaining rates,

with several modern supras fixing trips to china with I.Ore in the 18-20k rge for mid

August dates. Although no shortage of ships in the area, it seems the are more

cargoes available, partially due a small rise in the I.Ore price and increased buying

intrest. This has kept the supply/demand balance more or less in check. West Coast

India ships seemed to be valued a few thousand less than the East Coast ones for

trips to China and via RBCT. Short period enquiry was increased, with spot levels

coming off, chrts are starting to look at q4 where it seems both Charterers and

Owners are expecting a rise in rates, if only a modest one. The longer period market

was also active with quite a few vsls able and willing to do period of 1 up to 5 yrs.

Several modern supras were heard to have fixed for 11/13 months at 20-21k lvl for

ppt delivery India/Jpn Range. National Holiday in Singapore on Monday, so expecting

another slow start to the week.

ICP 07012814 All rights reserved Taizhou Maple Leaf